It’s May! Flowers are in bloom, kids are excited for the end of the school year, and we are celebrating National 529 Day!

You at least celebrated Financial Literacy Month with me in April, right?

If you have never celebrated 5/29 day, let’s start this year! The goal of National 529 Day is to bring awareness to families about the value of preparing for college and saving for our kids’ next (expensive) chapter through 529 plans.

What Is a 529?

What Is a 529?

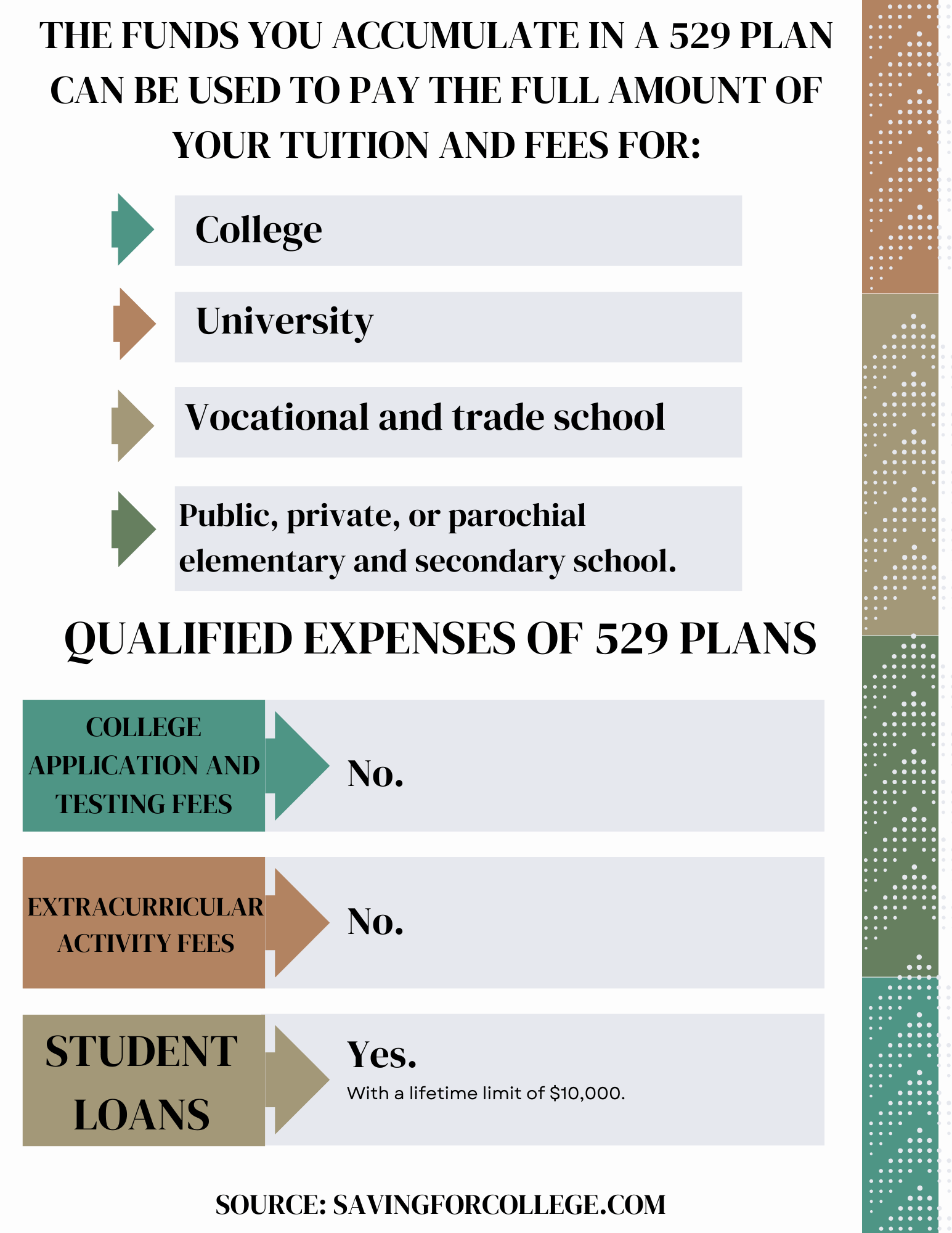

A 529 account is an investment account that provides tax benefits when used for qualified education expenses for the account’s beneficiary. Most people use 529 accounts to pay for college or higher education expenses, but as of January 1, 2018, 529 accounts can also be used for K-12 tuition (up to $10,000).

Many states are having statewide initiatives to encourage their residents to focus on saving. The College Savings Plan Network created this interactive map to show you what your state is doing for 5/29 Day. One item South Carolina is doing to celebrate is to provide any baby born on 5/29 a $529 grant into a Future Scholar Account!

529 Account Tax Benefits

1. Tax-deferred growth

The 529 account is opened and additional contributions are made with after-tax dollars (money we have already paid taxes on).

Money in the 529 account is invested in different mutual funds. If you are working with a Financial Advisor and they set up the 529 for you, they should provide you with recommendations on appropriate investments. If you are opening up the account directly with the 529 provider, you will need to choose an investment for your 529 account.

Any growth of the account is tax-deferred, meaning you do not pay taxes on the growth when it is happening.

2. Tax-free withdrawals

Withdrawals of money from 529 accounts are tax-free (as long as the withdrawn amount goes to pay for a qualified education expense). So you do not pay taxes on the growth of the 529 that you have been deferring since the account opened, as long as the withdrawn amount goes to pay for a qualified education expense.

Let’s say we open a 529 account with $1,000 for our eight-year-old daughter. After 10 years, it is time to start thinking about paying college tuition, and our 529 is now worth $5,000. If the money from the 529 goes to pay for qualified education expenses, the $4,000 that the account has earned over the past 10 years will be given to us tax-free and our $1,000 is returned back to us.

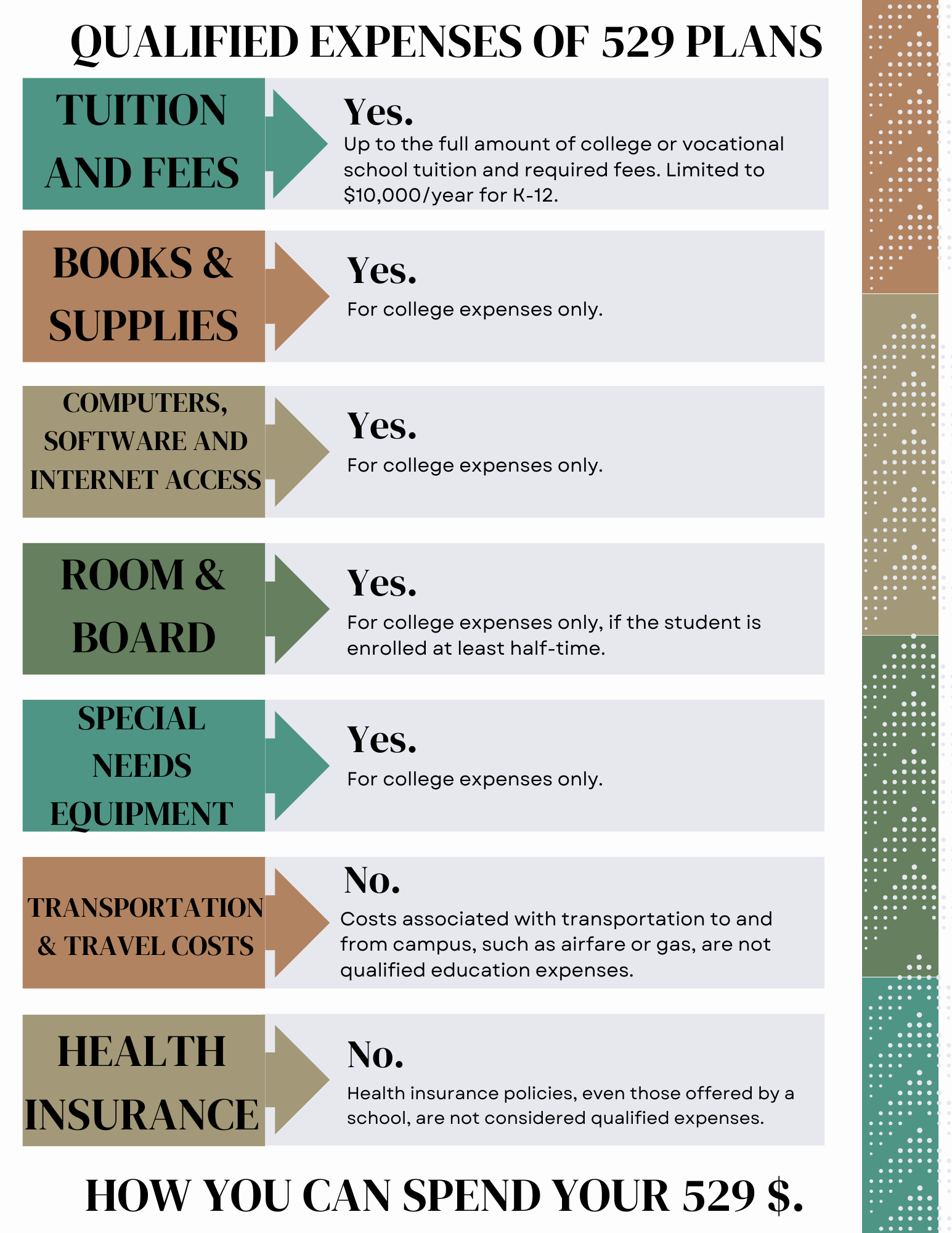

Since I’ve mentioned qualified education expenses a few times, the graph below shows you common education expenses, and if they are qualified or not.

3. State income tax deduction

3. State income tax deduction

South Carolina and 29 other states (including DC) allow 529 contributions to the state-sponsored 529 account to be fully deductible from your income.

When filing taxes, be sure to reduce your income by any 529 contributions to South Carolina’s Future Scholar 529 when calculating your South Carolina taxable income. Also, you can make 529 contributions for the prior year up until tax day. That means 2023’s contribution can be made until April 15, 2024!

South Carolina’s 529 program is called Future Scholar, which you can learn more about here.

Who Are the Parties of a 529 Account?

Owner: This person owns the account and makes the decisions regarding the account.

Beneficiary: This person is the student who the qualified education expenses will be provided for.

Successor Owner: This person becomes the owner of the 529 account if the original owner dies.

If You Do Not Use All the Money in Your Child’s 529

If you do not use all of the money in your child’s (beneficiary’s) 529 account because they did not attend college, you have a few options:

Option 1: Cash out the account. A heads up though, you will likely have taxes and penalties.

Option 2: Change the beneficiary of the account. Changing the beneficiary of a 529 will not impact the tax favorability as long as the new beneficiary is the original beneficiary’s family member. Which includes:

- Spouse

- Son, daughter, stepchild, foster child, adopted child, or a descendant

- Son-in-law, daughter-in-law

- Siblings or step-siblings

- Brother-in-law, sister-in-law

- Father-in-law, mother-in-law

- Father or mother or ancestor of either, stepmother, stepfather

- Aunt, uncle, or their spouse

- Niece, nephew, or their spouse

- First cousin or their spouse

Option 3: Roll up to $35,000 of a 529 account into a Roth IRA in the beneficiary’s name, tax and penalty-free. This new option becomes a reality starting in 2024, thanks to the passage of the SECURE 2.0 ACT in 2022. There are a few more rules of this act to consider, but for unused 529 dollars, this is certainly an exciting way to give your loved one a tax-free head start on their retirement savings.

If you didn’t use the full 529 amount because the beneficiary received education tax credits, received scholarships, attended a US military Service Academy, or passed away, the 10% tax penalty may be waived.

Although there are nuances to understand with 529s, they are a great way to save tax efficiently for your child’s education. Celebrate this 529 day by opening a 529 for your child, making an additional contribution to your beneficiary’s 529, or forward this article to another mom who may benefit from the information!

")

")

{kind=link}